ZeroHedge by Tyler DurdenMon, 12/02/2019 – 08:33

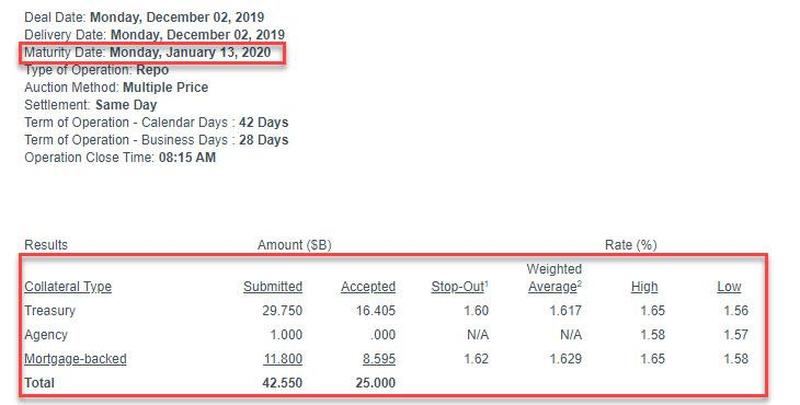

One week after the Fed’s first 42-day term repo which for the first time allowed dealers to lock in funding into the new year and which was 2x oversubscribed, confirming a growing scramble for year-end funding, traders were keenly looking ahead to the result from today’s second 42-day repo which matured on January 13. And, as we noted last week, year-end liquidity fears remain front and center as the $25 billion operation proved to be roughly 40% below the required size to satisfy all liquidity demands.

Dealers submitted $42.550BN in bids for the 42-day op ($29.750BN in Treasurys, $1BN in Agency, $11.8BN in MBS paper), resulting in an oversubscription of the $25BN in available repo.

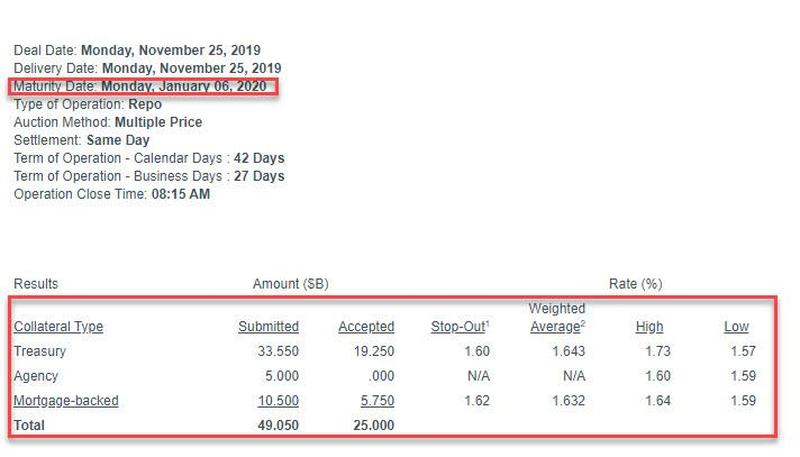

This was modestly below the $49.050 billion submitted in the first 42-day repo operation conducted on November 25:

It remains a key question for funding markets why, even with QE4 in place and now daily overnight and short-term repo operations in place, banks continue to rush to lock in year-end liquidity, where some fear a similar explosion in overnight repo rates as was observed on Dec 31, 2018 when General Collateral soared amid a widespread liquidity shortage. Indeed, as Bloomberg put it, “even with the Fed’s commitment to continue providing liquidity to the financial system around year-end, the market is still showing concerns. This is due to banks’ year-end balance-sheet constraints related to capital surcharges and other regulatory requirements.”

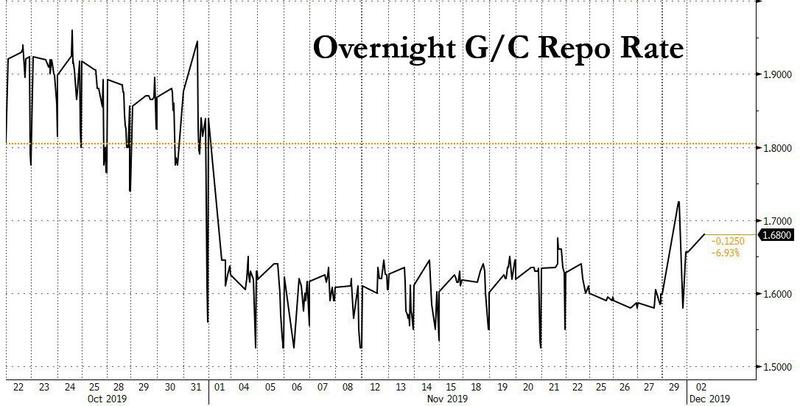

The clearest indication that despite the massive liquidity injections that have taken place since mid-September liquidity remains scarce was today’s initial print in the overnight General Collateral rate, which rose from 1.60% to 1.68%, the highest since the Fed cut rates on Oct 31.

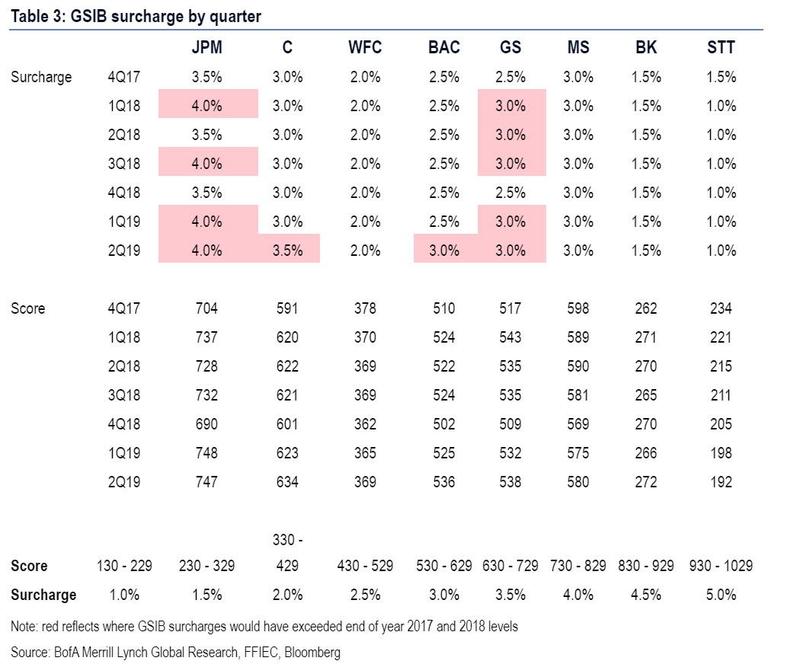

So what is it about quarter and year-end that is forcing banks to shore up their balance sheets with liquidity? As a reminder, while most US bank have a GSIB surcharge of around 2%-3%, JPMorgan remains an outlier – and is perceived as the “riskiest” bank – with its 4.0% surcharge. It’s also the reason why the bank has been quietly pulling liquidity away from funding markets ahead of quarter-end periods.

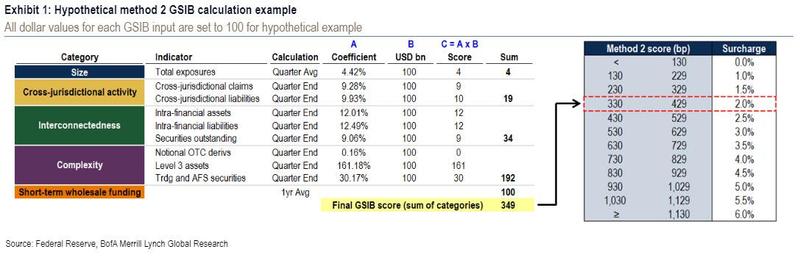

For those curious how the Fed calculates the GSIB surcharge, Bank of America provided the following handy schematic:

Two weeks ago, when commenting on why it expects to see sharp year-end liquidity pressures, BofA said that funding markets are currently very stable but the bank sees risks of repo pressure into year-end, as the Fed faces two funding issues into Y/E:

- a low level of reserves requiring ongoing large Fed repo injections

- dealer repo intermediation constraints stemming from the GSIB surcharge.

The way these issues are linked is through the Fed’s short-term repos; Fed repos pressure dealer balance sheets larger while GSIB constraints encourage dealers to shrink the overall size of their market making activities.

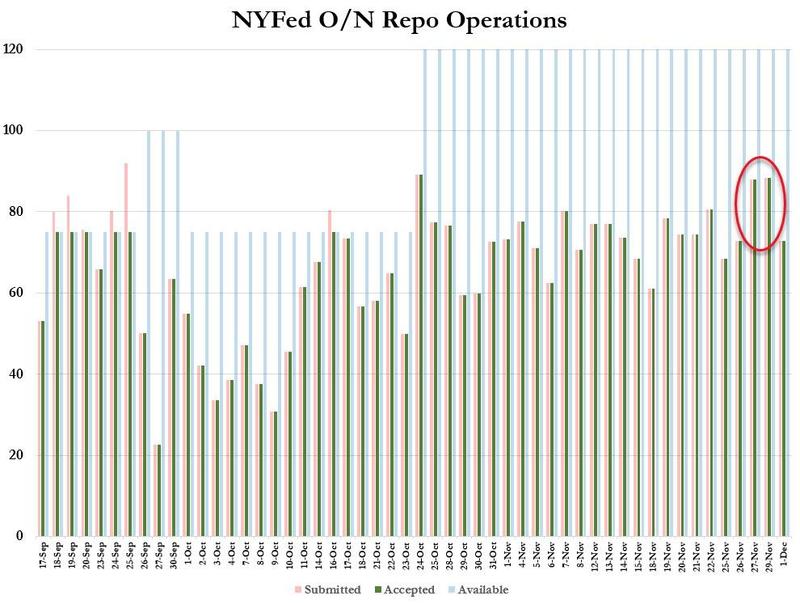

Separately, and in keeping with the recent tradition, the Fed also completed an overnight repo operation, which however showed less funding demand, as “only” $72.9 billion in securities were pledged in exchange for overnight liquidity with the Fed, well below the limit of $120 billion. Yet another troubling observation: while many have expected the total notional on overnight repos to decline over time, the daily use of the overnight repo has stabilized in the $60-$80 billion range and has failed to decline over the past month.