Lustrous, Semi-PL

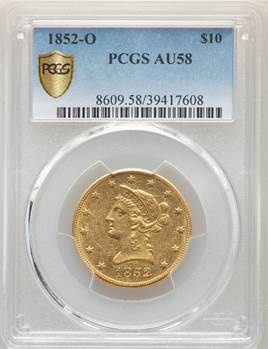

With their energies directed mostly toward the production of double eagles, New Orleans Mint officials struck a paltry 18,000 ten-dollar gold coins in 1852. In 2006, Doug Winter, who called this issue “one of the rarest No Motto eagles,” estimated 80 to 90 coins survived in all, including two to four Uncirculated coins. Today, NGC shows two in Mint State (one in MS60 and one in MS61) on their population report, while PCGS shows one in MS60, with none higher. The PCGS population is only 4 with 3 higher (two AU58+’s and the aforementioned MS60).

Offered at $26,900 delivered

We do business the old fashioned way, we speak with you. Give us a call for price indications and to lock trades.

(800) 257.3253

9:00 AM – 5:00 PM CST M-F

Private, Portable, Divisible Wealth Storage

Price is based on payment via ACH, Bank Wire Transfer or Personal Check.

Major Credit Cards Accepted, add 3.5%

Offer subject to availability.

, in Verkhnyaya Pyshma, Russia, on Thursday, July 30, 2020. Gold surged to a fresh record Friday fueled by a weaker dollar and low interest rates. Silver headed for its best month since 1979., Bloomberg")