By StefaniaSpezzati, Donal Griffin, and Viren VaghelaNovember 28, 2019, 10:36 AM CST Updated on November 29, 2019, 2:35 AM CST

Morgan Stanley fired or placed on leave at least four traders over an alleged mismarking of securities that concealed losses of between $100 million and $140 million, according to people with knowledge of the matter.

The firm is investigating the suspected mismarking, which was linked to emerging-market currencies, said the people, who asked not to be identified as the details are private. Tom Walton, a spokesman for the New York-based bank, declined to comment.

The traders who have been identified as part of the probe include Scott Eisner and Rodrigo Jolig, both based in London, and two senior New York-based colleagues, Thiago Melzer and Mitchell Nadel, the people said. Eisner, Jolig, Melzer and Nadel didn’t respond to requests for comment. Their ultimate employment status isn’t yet clear, but at least some of them are leaving the bank, the people said.

Melzer was given responsibility for foreign exchange and emerging-markets Americas trading in March, while Nadel runs macro trading in the Americas, including rates and currencies. Eisner was managing orders for the Central and Eastern Europe, Middle East and Africa currency book, known as CEEMEA, according to his LinkedIn profile.

In so-called mismarking, the value placed on securities doesn’t reflect their actual worth. The scope of the probe at Morgan Stanley includes currency options that give buyers the right to trade at a set price in the future, enabling them to both speculate and hedge against potential losses. Dealing in foreign-exchange options surged 16% to $294 billion per day in April, according to the most recent data from the Bank for International Settlements.

Morgan Stanley’s currency options desk has struggled this year amid a slump in the volatility that generates profits for traders, even in the more unruly emerging markets, according to a person with knowledge of the performance. The JPMorgan Global FX volatility index trades at the lowest since the summer of 2014.

Third Quarter

The Wall Street firm booked some of the losses in the third quarter, one of the people said. Morgan Stanley reported a 21% increase in overall fixed-income trading revenue, a result that was “partially offset by a decline in foreign exchange,” according to its third-quarter earnings presentation.

The probe shows “the amount of effort still needed in these large organizations to reduce episodes of misconduct,” said Angela Gallo, a finance lecturer at Cass Business School. “The frequency of misconduct cases in the U.S. and Europe in recent years speaks very loudly that more fundamental changes are required.”

It has been a turbulent week for securities firms in London and New York after Citigroup Inc. was fined 44 million pounds ($57 million) by the Bank of England for years of inaccurate reporting to regulators about the lender’s capital and liquidity levels. The incidents point to weak internal controls at investment banks a decade on since the financial crisis.

Natixis SA, the French lender roiled by risk-management problems since last year, has suspended a senior trader at a subsidiary in New York pending an internal investigation, Bloomberg News reported this week.

Officials at the French bank are reviewing issues around how some of the senior trader’s transactions have been recorded, the people said. The bank is also examining how he managed his portfolio of trades, they said, requesting anonymity as the details aren’t public.

— With assistance by Silla Brush(Updates with additional details in final paragraph.)

Tad Rivelle, Chief Investment Officer of the Californian bond house TCW, doubts that the Central Banks can prevent the impending economic downturn. He spots increasing signs of stress in the credit sector and recommends holding safe assets to be prepared for turmoil in the financial markets.

Mr. Rivelle, who rarely gives interviews, views the prospects on the financial markets with skepticism. In his opinion, it’s clear that the business cycle is in its final stages. He warns that the power of unconventional monetary policy is largely exhausted and nervousness in the credit sector is growing.

Against this background, he advises a defensive calibration of the portfolio and a careful approach when it comes to security selection – especially in the investment grade segment where many companies are more leveraged than their rating indicates.

Mr. Rivelle, the rally in stocks has lost some of its momentum recently. Nevertheless, the S&P 500 is near its all-time high. What’s your take on the current market environment?

We’re very skeptical of taking risks in this market since there is fairly abundant evidence that we’re in a late cycle type of environment. Equity valuations are largely following the script of the central banks: The central banks say dance, and the equity market is dancing. In contrast, debt investors increasingly say: «There is nothing in it for me to get on the dance floor because as a debt investor, all I get back is a 100 cents on the dollar». We’re the asset class that’s always at risk of loss. The Federal Reserve can say and do whatever it wants. But if it can’t get the private sector to follow through with cheap financing and debt markets become skeptical of providing favorable financing, I don’t know where you go with that.

Globally, there’s around $ 12 trillion in negative yielding debt. How do you approach such a market as a veteran fixed income investor?

It’s an absurdity and an artificial condition. For instance, a Swiss company like Nestlé finds itself in some kind of financial paradox: They can issue negative yielding debt in Swiss francs and then use the proceeds to buy back their own equity. If you want to reflect on this philosophically: Why have any equity at all? You could just buy it all back. That leads to the next observation: Your assets theoretically are producing benefits and your liabilities are producing benefits, too. This would imply there’s no cost running your business at all. This is obviously a hint that markets didn’t get to negative interest rates through a negotiation process between borrowers and lenders. Rates were pushed off the cliff by the central banks.

What are the consequences of these artificially low interest rates?

The collective and extraordinary expansion of central bank balance sheets has powered the «bull market in everything». But these absurd policies aren’t going to work for the long term. In this cycle, the Zeitgeist has been that the central banks have the capacity to maintain growth and prosperity. In others words: If you control the financing right to corporations and consumers, you can make the economy grow forever. This flies in the face of common sense. Economics used to always be about the idea that you need to incentivize producers to make efficient choices. If you give them the right incentives, they will raise the bar in terms of value addition and growth over time. But when you artificially chose your rates, you are doing the opposite. You’re causing bad choices by definition.

Where are such bad choices evident today?

The low rate environment has created excesses in a lot of areas. It has driven up asset prices, and as you drive up enterprise multiples, you drive up leverage multiples. Look at private equity: The best idea that most institutional investors say is in their portfolio is private equity. That’s strange since the whole concept of private equity is basically that you buy up businesses, you put a lot of leverage underneath them, you don’t mark things to market – at least not the same way as the public markets do – and you create this illusion of low volatility investments. So you have a system where company managers get enabled to say ridiculous things to their investors like: «We don’t care about profits». I don’t think we would have a company like WeWork if we didn’t have an environment where investors are thinking that they need to invest in a fairy tale because they can’t earn a return any other way.

What’s your take the WeWork disaster?

WeWork was one of these situations hiding in plain sight. There were plenty of people who expressed skepticism. Yet, you had money center banks playing along, making loans and adding to the credibility of it. So you had a fairy tale: You had a $47 billion unicorn two or three months ago that now had to be rescued. I’ll go further: If SoftBank didn’t rescue WeWork, would you really want to find out what the lawsuits are going to discover when the Limited Partners sue SoftBank? When they ask: «How did we get to $47 billion, exactly?» And while you’re at it, you might be even doing that in a court in Riyadh. So maybe this point, the best course of action is just to pay everybody off and then figure out what to do.

Where are other disasters hiding in plain sight?

When you get to the last phase of the cycle, you need to be thinking about what could go wrong, because there is very little probably that’s going to go right. Today, a lot of carnage has come to the fracking area. There are a lot of E&P capital structures that are evidently no longer financeable in the capital market. A lot of these businesses are probably going into bankruptcy. Also, you see stress in automotives, in semiconductors and in retail. What’s more, it’s fair to say that the bank loan market represents one of the significant risks out there.

What are red flags investors should watch out for?

The number of high yield credits trading at spreads over a thousand basis points over treasuries has been rising all year long. Also, you’re seeing a lot more volatility in the leveraged lending space. Credit Investors increasingly are firing first, and ask questions later. This speaks back to another of the excesses in this cycle. Traditionally, the deal was that if you are a leveraged company, you were given two choices in the debt markets: Door number one, you can show the world what your financials are, adhere to the public standards, issue high yield bonds and report to the SEC and your debt investors what’s going on. Door number two: If you don’t want to show your numbers you had to get your hands tied behind your back. The lenders will give you the money but they won’t let you do much of anything with it because they want to make sure you’re not doing something stupid while they can’t watch you.

And what’s going on in this cycle?

This cycle, we have moved to an environment where what was a covenant heavy bank loan market has become a covenant light bank loan market. As a debt investor, you don’t have transparency and you have no ability to constructively restrict what management is doing. Private equity plays into this dynamic because it has used its market power to negotiate on behalf of its portfolio companies. So we’ve seen a worsening of covenants and credit agreements. Some of this relates back to a basic dynamic that the Fed and other central banks have put their hand on the scale: They’re basically communicating that they want to make it so easy for borrowers that lenders are saying: «Cash is burning a hole in my pocket. I need to do something with it.»

How does this end?

This is how it all ends badly. Think about the DNA of markets. Let’s say, you want to buy a house. In a red-hot market, you show up at the first day and there’s twenty people looking to buy. You want to do your due diligence and ask about the foundation, the roof and maybe the crazy neighbor. Finally, you get hold of the seller and he’s like: «I don’t have time. I’m not answering your questions. The only thing I want to hear from you is how much over the full offer price you want to pay.» That’s the way the credit markets were in 2017. «Drive-by» deals were done and investors like ourselves got the call in the morning saying: «Company XYZ is raising $ 500 million, you’re in or you’re out?» So no time for due diligence.

That doesn’t sound like prudent behavior.

Now, fast forward a couple of years and suppose you’re in a stone-cold housing market. You list your house, you wait three weeks and finally, some barely qualified buyer walks through the door and wants to know about your foundation, your roof and the crazy neighbor. After you’re done answering his questions, he’s got more and more questions because he recognizes intuitively that every time you can’t answer a question, he can make a worse case assumption and use it as justification to knock your price down. So suddenly the market has become completely illiquid and very hostile.

At which stage are we in the credit markets today?

Generally, if you’re involved in a bank loan that doesn’t have the parameters a CLO would naturally buy, the sponsorship is thin. If everything is fine, you probably won’t experience a lot of volatility. But miss your earnings or communicate some bad news and investors drop challenged credits like «hot potatoes.» That’s logical because your business has been operating in the dark. You haven’t told your lenders anything for years. Now, the only news you’re giving them is bad news. So they have to assume that this bad news hasn’t just happened yesterday, but there are deeper ongoing issues. They want out, but there is no bid on the other side. That’s why a liquidity crisis is all but inevitable.

How long until these developments evolve into a bigger issue for the financial markets?

We thought it was going to happen two years ago. Credit markets look late cycle, manufacturing looks pretty late cycle and corporate profitability, as well. So the proliferation of negative rates may also suggest that central bank policy has reached exhaustion. It’s almost like negative rates are the last thing central bankers are trying to make it work.

What are the chances of a recession against this backdrop?

It’s a little hubristic to say we’re going to have a recession in the next twelve months. What’s not hubristic is to say that these policies are not working and we will inevitably have a recession. Didn’t we try this at least once or twice before? Didn’t the Soviet Union have zero percent interest rates? Didn’t they have recessions? Maybe it wasn’t visible in the official statistics, but their recessions were manifested by longer lines at food stores.

What have zero percent or negative interest rates to do with that?

Artificial asset prices distort resource allocation and growth. Look at the fact that Sears and Kmart are for all intents and purposes just about to disappear on the scrap yard of history. All the resources invested in stores, labor and capital, are worthless. So the faster you get rid of it, presumably the better off you’re ultimately going to be. Recessions are not optional, they are inevitable. It’s the process in which it’s all getting washed out and rearranged. It’s like: «Don’t you want to get to the passing lane eventually? Or do you want to be stuck in the right line because you’re afraid of change?» Eventually you have to do it anyway.

An important piece of the puzzle is the US consumer. How healthy are households in the United States financially?

The US consumer is divided: You have the middle- and upper-class consumer, which seems to be in fine shape at the moment. You wouldn’t expect differently because consumer proclivity to buy is a function of income, employment and housing prices. So middle class people in general feel more secure with employment as high as today and their house worth 20% more versus what it was ten years ago. On the other hand, the subprime consumer is more credit dependent and metrics there are not really good. We’re seeing deterioration in delinquency rates and charge-offs for the lower range of credit counterparties. The problem is, that this is where a lot of growth ultimately comes from, from the marginal buyer.

What does it mean in terms of Fed policy? Are more rate cuts coming down the road?

Receive a daily recap featuring a curated list of must-read stories.

Let me be maximally charitably to the Fed: They have no backing by elected officials from either party to do anything but lower rates in response to incremental economic weakness. So it’s fair to say that if the economy weakens they will lower rates more, regardless of what they say. It won’t happen this year, I presume. But I guess in 2020 they’re going to cut rates again. We invented central banks because we figured out that the banking system, if left to its own faith, is too volatile and that we need a state sponsored institution to cushion the blow. But somehow, we went from there to the Fed buying $ 60 billion of T-Bills a month, calling it not Quantitative Easing, and central banks in Europe and Japan imposing negative rates.

What’s the yield on the ten-year treasury going to be in a year from now?

I would say somewhere around where it is today, between 1.5 and 2%. But that’s just a wild guess. It’s a question of timing and causation: If this becomes a global led downturn you have to assume that US rates are going lower. But you can also imagine other scenarios. US rates being above overseas rates has brought huge capital inflows and people are getting very used to the idea that these capital inflows will always hold down US rates. But what’s going to happen when these flows reverse for who knows what reasons and US rates go up?

What should a prudent investor do under these circumstances?

You should adapt your underwriting standards to the kind of environment that you are in. So, beginning a couple of years ago, we adopted our underwriting standards to be much more careful with respect to the types of risks we’re taking throughout our whole portfolio. In other words: Stay vigilant, focus on staying liquid, focus on safe assets and wait for volatility to present opportunity.

So how does a robust bond portfolio look?

It was Benjamin Graham pointing out that bond selection is a negative art. That’s especially true in the late cycle. Cycles die in large measure because capital gets tied up in unprofitable enterprises. So you need to think long and hard about what claims are breakable and can suffer catastrophic and permanent price declines. There may be a time to own breakable assets, but after they break and not before.

What are such breakable assets today?

There will be plenty of breakable assets and a lot of them will be in the high yield and bank loan market. Some maybe even in the investment grade market. Today, 11% of investment grade issuers are levered more than five times, an 27% are levered more than four times. In this context, you could make a pretty good case that 50% of BBB debt would have a high-yield rating based on leverage alone.

Where are better places to invest?

We’re counselling to divide your assets between bendable assets and riskless assets for the liquidity issues that we’re going to encounter. I would put treasuries and agency mortgages as the risk-off, liquid part of the portfolio. You can’t retire on them or really do anything with it. But you can own them tactically to finance the expansion of your bendable assets: Assets that are exposed to mark-to-market risk, meaning they go up and down, so they may be exposed to liquidity risks. But they provide you yield today and their claims will survive into the next cycle, if you have done your categorization right.

What are attractive bendable assets?

Bendable is what we refer to as true investment grade credit. Also, AAA-rated commercial mortgage-backed and asset-backed securities as well as senior non-agency residential mortgage-backed securities. Stuff that we’re invested in obviously. In some cases, AAA-rated CLO tranches can potentially make some sense, too. And, if you can find them, some high yield securities maybe, or a few emerging market securities. You try to find companies with a wide enough moat around what they’re doing, like regulated utilities as long as they’re not in California where you have a special environment with damage claims from wildfires.

This example exceeds the quality of almost all other PL 1881-S dollars. There are some splashes of delicate golden toning (which are far more subtle than seen in our images) around the borders, but most of each side is brilliant. The reflectivity of the fields is captivating, but the true hallmark of this coin is its state of preservation. Liberty’s cheek is essentially flawless. If you like it, based on our pictures, you will love it in hand. Tied with four others for the highest graded by PCGS.

Offered at $9,775 delivered

We do business the old fashioned way, we speak with you.

The twenty cent denomination is one of the great failures in American numismatics. There was never any great need for it. Its use was limited to the West, where consumers would often pay a quarter for items worth a bit (one reale, or 12.5 cents) and receive a dime back in change. Copper did not circulate in the Pacific states, so consumers were often shortchanged by two cents. The twenty cent denomination was suggested by Nevada Senator John P. Jones as a way of solving that problem. It never caught on, and the denomination was abandoned for circulation in 1876, one year after it was first introduced. The NGC population I sonly 8 with 1 higher.

Offered at 20,750 delivered

We do business the old fashioned way, we speak with you.

The 1903 Liberty eagle is a great condition rarity in MS66, somewhat surprising considering the mintage was 125,800 pieces and it is frequently encountered in lower grades. There is only one other MS66 certified — a PCGS coin (which auctioned in 2012 for $22,325). The strike is sharply detailed throughout, and the frosty lemony-gold surfaces are nearly perfect, aside from a lone mark behind Liberty’s eye that determines pedigree.

Offered at $15,525 delivered

We do business the old fashioned way, we speak with you.

Here is a rare opportunity for a complete, well matched PCGS MS65 set of Liberty Nickels. Each coin exhibits light to medium patina, with none being dark or unattractive. Please note that what looks to be a humongous scratch on the 1912-S, is a scratch on the holder, not the coin. Additionally, the 1885 and 1886 – the two most valuable coins in the set – are highly lustrous and eye-appealing.

Offered at $30,475 delivered

We do business the old fashioned way, we speak with you.

An adequate mintage of 6.9 million Morgan dollars was accomplished in 1901, but the issue is more elusive than the respectable production total would suggest, especially in high grade. Many coins were released into circulation and suffered heavy wear and attrition over the years. Of the coins held in government storage, many were probably melted in 1918, under the provisions of the Pittman Act. Relatively few high-quality examples were saved by contemporary collectors. Today, the 1901 Morgan dollar can be found in circulated grades without much difficulty, while lower Mint State specimens are scarce, and high grade examples are rare. Lighter and brighter than seen in our images.

Offered at $8,860 delivered

We do business the old fashioned way, we speak with you.

No official records have surfaced to document the striking of Proof High Reliefs. However, David Akers, and many other numismatists have gone on record as believing a small number were struck, and NGC has certified some with specific die characteristics, as proofs (PCGS does not recognize the existence of proof High Reliefs at this time). According to Scott Schechter/NGC: The coins exhibit crisp strikes and distinctive satin surfaces, with heavy, swirling die polish lines, and are struck from the earliest state of one specific die pair. The most easily recognized feature is the edge lettering, as all proofs were struck using the same collar used to strike the Ultra High Relief double eagles, with a raised collar-segment line between the S in PLURIBUS and a star. This example is lighter and brighter than it appears in our images.

Offered at $60,375 delivered

We do business the old fashioned way, we speak with you.

The 1921 Saint-Gaudens double eagle is one of the major rarities in the series, despite an innocuous-sounding mintage of 528,500 coins. But the issue is the only gold coin the United States struck during the year. The date was not exported for international trade; neither did it circulate in the United States. Rather, the coins stayed in Treasury vaults until the 1930s, when they were melted in the great extinction event of the era, the Gold Recall of 1933. Examples are absent in overseas holdings returned to the States, and no domestic hoards have been uncovered. It is likely that no more than 175 examples of the issue survive in all grades.

Offered at $78,950 delivered

We do business the old fashioned way, we speak with you.

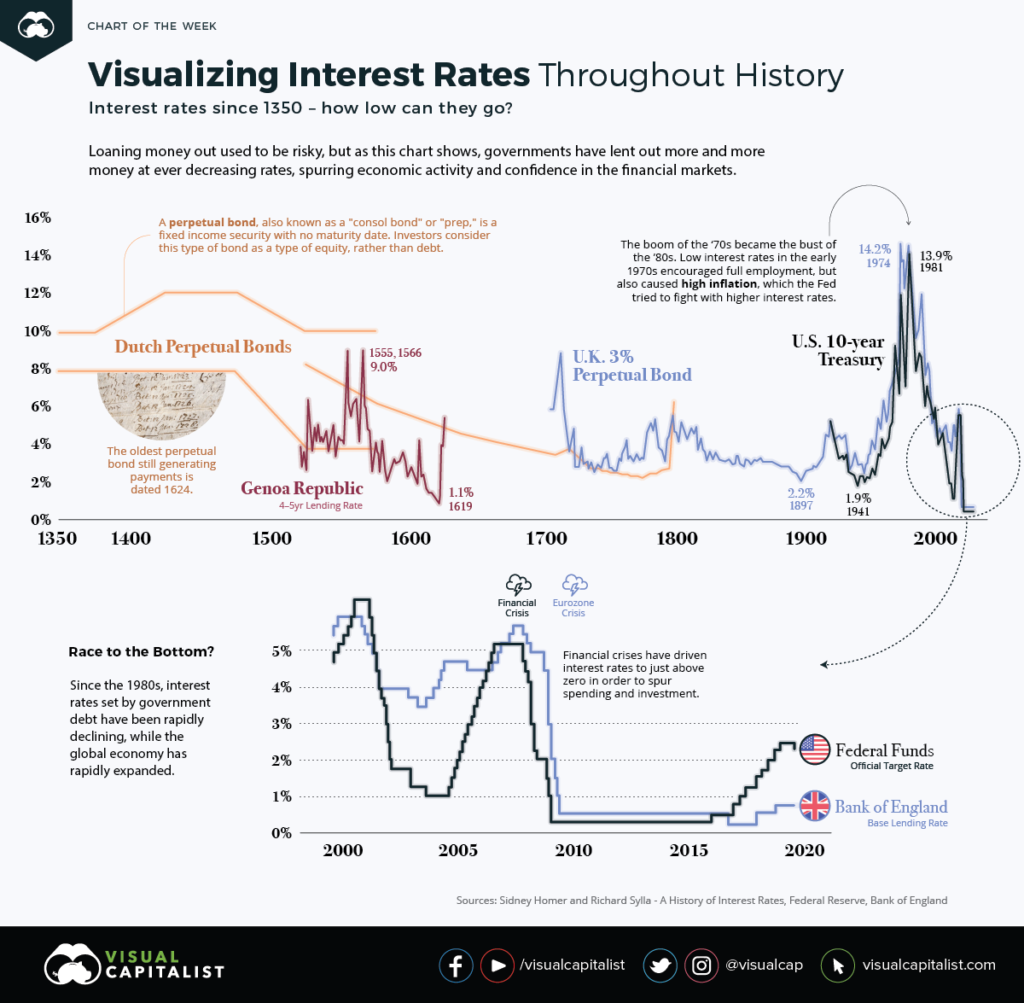

Today, we live in a low-interest-rate environment, where the cost of borrowing for governments and institutions is lower than the historical average. It is easy to see that interest rates are at generational lows, but, as Visual Capitalist’s Nicholas LePan notes below, did you know that they are also at 670-year lows?

This week’s chart outlines the interest rates attached to loans dating back to the 1350s. Take a look at the diminishing history of the cost of debt—money has never been cheaper for governments to borrow than it is today.

Courtesy of Visual Capitalist

The Birth of an Investing Class

Trade brought many good ideas to Europe, while helping spur the Renaissance and the development of the money economy.

Key European ports and trading nations, such as the Republic of Genoa or the Netherlands during the Renaissance period, help provide a good indication of the cost of borrowing in the early history of interest rates.

The Republic of Genoa: 4-5 year Lending Rate

Genoa became a junior associate of the Spanish Empire, with Genovese bankers financing many of the Spanish crown’s foreign endeavors.

Genovese bankers provided the Spanish royal family with credit and regular income. The Spanish crown also converted unreliable shipments of New World silver into capital for further ventures through bankers in Genoa.

Dutch Perpetual Bonds

A perpetual bond is a bond with no maturity date. Investors can treat this type of bond as an equity, not as debt. Issuers pay a coupon on perpetual bonds forever, and do not have to redeem the principal—much like the dividend from a blue-chip company.

By 1640, there was so much confidence in Holland’s public debt, that it made the refinancing of outstanding debt with a much lower interest rate of 5% possible.

Dutch provincial and municipal borrowers issued three types of debt:

Promissory notes (Obligatiën): Short-term debt, in the form of bearer bonds, that was readily negotiable

Redeemable bonds (Losrenten): Paid an annual interest to the holder, whose name appeared in a public-debt ledger until the loan was paid off

Life annuities (Lijfrenten): Paid interest during the life of the buyer, where death cancels the principal

Unlike other countries where private bankers issued public debt, Holland dealt directly with prospective bondholders. They issued many bonds of small coupons that attracted small savers, like craftsmen and often women.

Rule Britannia: British Consols

In 1752, the British government converted all its outstanding debt into one bond, the Consolidated 3.5% Annuities, in order to reduce the interest rate it paid. Five years later, the annual interest rate on the stock dropped to 3%, adjusting the stock as Consolidated 3% Annuities.

The coupon rate remained at 3% until 1888, when the finance minister converted the Consolidated 3% Annuities, along with Reduced 3% Annuities (1752) and New 3% Annuities (1855), into a new bond─the 2.75% Consolidated Stock. The interest rate was further reduced to 2.5% in 1903.

Interest rates briefly went back up in 1927 when Winston Churchill issued a new government stock, the 4% Consols, as a partial refinancing of WWI war bonds.

American Ascendancy: The U.S. Treasury Notes

Receive a daily recap featuring a curated list of must-read stories.

The United States Congress passed an act in 1870 authorizing three separate consol issues with redemption privileges after 10, 15, and 30 years. This was the beginning of what became known as Treasury Bills, the modern benchmark for interest rates.

The Great Inflation of the 1970s

In the 1970s, the global stock market was a mess. Over an 18-month period, the market lost 40% of its value. For close to a decade, few people wanted to invest in public markets. Economic growth was weak, resulting in double-digit unemployment rates.

The low interest policies of the Federal Reserve in the early ‘70s encouraged full employment, but also caused high inflation. Under new leadership, the central bank would later reverse its policies, raising interest rates to 20% in an effort to reset capitalism and encourage investment.

Looking Forward: Cheap Money

Since then, interest rates set by government debt have been rapidly declining, while the global economy has rapidly expanded. Further, financial crises have driven interest rates to just above zero in order to spur spending and investment.

It is clear that the arc of lending bends towards ever-decreasing interest rates, but how low can they go?