The Mint struck 154 proof quarter eagles in 1907, marking the end of the Liberty Head type. About two thirds of these exist today, and many in remarkable states of preservation. The end of the type may have prompted more examples to be preserved than in other years, but the unappealing matte proofs of the following year likely also spurred collectors to more carefully preserve the last of the brilliant mirror proofs.

This coin serves as a good example that the phrase “A picture is worth a thousand words” is not always true. In this particular instance, the coin is more yellow-gold (as opposed to orange-gold) than shows in our images. In addition to that, if you tilt it even slightly, you will see considerably more obverse frost and contrast than is apparent in our photo. Said differently, this example is absolutely stunning! The PCGS population is 9 with 9 higher.

Offered at $23,500 delivered

We do business the old fashioned way, we speak with you.

The 1856 Flying Eagle cent was originally issued as a pattern, to demonstrate the new small-size copper-nickel design. Large numbers were struck to showcase the design to Congressmen and other VIPs, in both proof and business-strike format. Most of the proofs were from the Snow-9 dies, characterized by a center dot under the upper-left serif of the N in CENTS. The issue has always been collected by Flying Eagle-Indian cent specialists and pattern collectors alike. Only seven have been graded higher by PCGS.

Offered at $33,485 delivered

We do business the old fashioned way, we speak with you.

Most of the S-Mint double eagles coined in 1862 entered circulation, and today the average certified grade is just below AU50. The S.S. Brother Jonathan and S.S. Republic treasure recoveries contributed 190 examples to the numismatic marketplace. Despite the appearance of those coins in the last two decades, this issue us still quite rare in uncirculated grades. The one offered here is noticeably more lustrous and attractive than seen in our images. The current NGC population stands at 11 with 36 higher.

Offered at $9,400 delivered

We do business the old fashioned way, we speak with you.

The year 1855 saw heavy double eagle production on both coasts, with 364,666 pieces struck at Philadelphia and nearly 880,000 coins minted at San Francisco. Do not be misled by those figures! The Philadelphia coins are much scarcer than their S-mint counterparts across all grade levels, and Mint State representatives are quite rare. In fact, PCGS and NGC combined have graded fewer than 50 pieces in all uncirculated grades.

Offered at $10,575 delivered

We do business the old fashioned way, we speak with you.

The 1859 Liberty double eagle claims one of the lowest business-strike mintages of any Type One double eagle from the Philadelphia Mint, at a meager 43,597 pieces. The small business-strike production was largely ignored by contemporary numismatists and few high-quality pieces were preserved for posterity. The 1859 is an elusive issue in all grades today, and most survivors grade in the VF-XF range. This representative is considerably brighter and more lustrous in hand. Not surprisingly, the PCGS population stands at just 18 with 24 higher.

Offered at$17,625 delivered

We do business the old fashioned way, we speak with you.

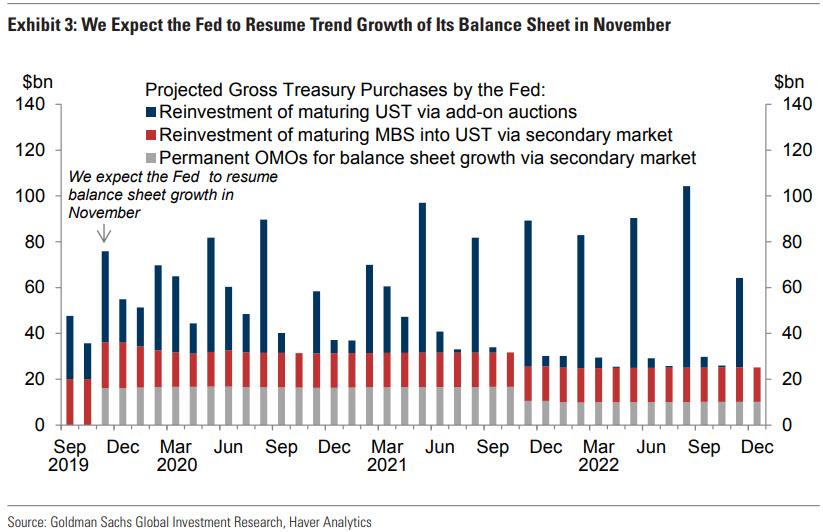

Yesterday we reported that Goldman now expects the Fed to restart Permanent Open Market Operations, i.e., bond purchases, i.e., QE some time in November. For those who missed it, Goldman assumes a roughly $15bn/month rate of permanent OMOs, “enough to support trend growth of the balance sheet plus some additional padding over the first two years to increase the size of the balance sheet by $150bn”, in the process restoring the reserve buffer and eliminating the current need for temporary OMOs.

That strategy would result in balance sheet growth of roughly $180bn/year and net UST purchases by the Fed (the sum of the red and grey bars) of roughly $375bn/year over the next couple of years.

However, assuming Goldman is correct, there would be a little over a month before such POMO returned to permanently increase the size of the Fed’s balance sheet, potentially resulting in a continued liquidity shortage for the next 6 or so weeks.

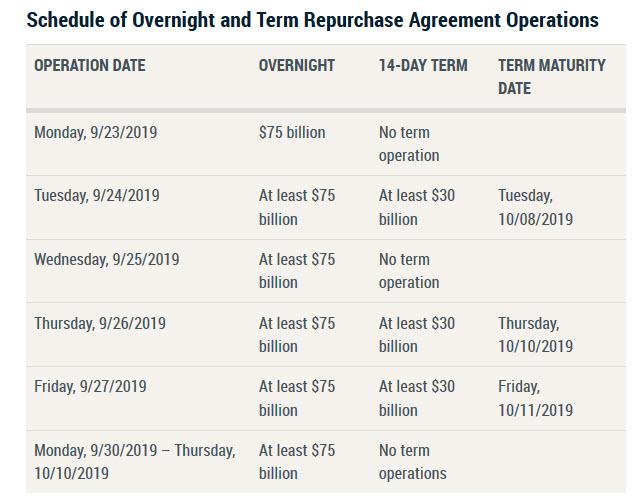

Which probably explains why moments ago, the Fed surprised market watchers who were expecting the Fed to continue conducting only overnight repos, but announcing that not only would it conduct overnight $75 Billion repos every day from Monday until Thursday, October 10, but it would also introduce 2 week term repos with a total size of “at least $30 billion” for the first time since the financial crisis.

This is what the NY Fed said moments ago in a statement regarding repurchase operations:

In accordance with the Federal Open Market Committee (FOMC) directive issued September 18, 2019, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct a series of overnight and term repurchase agreement (repo) operations to help maintain the federal funds rate within the target range.

The Desk will offer three 14-day term repo operations for an aggregate amount of at least $30 billion each, as indicated in the schedule below. The Desk also will offer daily overnight repo operations for an aggregate amount of at least $75 billion each, until Thursday, October 10, 2019. Awarded amounts may be less than the amount offered, depending on the total quantity of eligible propositions submitted. Securities eligible as collateral include Treasury, agency debt, and agency mortgage-backed securities. Additional details about the operations will be released each afternoon for the following day’s operation(s).

The proposed schedule of upcoming overnight and term repos is as follows:

What are the implications from the above? There are several, and they are concerning.

First, by expanding the “plumbing” arsenal from just overnight repos to three “at least $30 billion” term repos for at least one week, the Fed is telegraphing that it was expecting the overnight repo oversubscription situation to continue indefinitely, which in turn suggests that the NY Fed is worried the dollar funding shortage may continue, and as such it is expanding its toolbox to release up to at least $90 billion in additional liquidity, which together with the $75 billion in rolled overnight repo, would unlock as much as $165 billion in additional liquidity at the end of next week.

As a reminder, Goldman calculated that the Fed’s restart of POMO would increase the size of the Fed’s balance sheet by $150 billion, which is almost in line with the $165 billion in liquidity that the Fed will unlock in the form of “sterilized” repo operations. In other words, the Fed just confirmed that the reserve shortfall is likely at least $165 billion, and in doing so, it also indicated that a long-term solution will need to be reached, one which almost certainly will validate the prediction that QE/POMO is coming in November.

Second, as noted earlier, whereas overnight repo rates have stabilized, term repo rates remain elevated, especially those terms that capture either quarter or year-end, times when the US financial system traditionally suffers from a material liquidity shortfall: “The term market is still quite choppy,” confirmed Subadra Rajappa, head of rate strategy at Societe Generale in New York. As Bloomberg further adds, for the 10-year note futures contract versus the cheapest-to-deliver Treasury security to Dec. 31, the basis Friday implied a term repo rate of about 2.15%. While that’s down from about 2.40% late Thursday, it remains above the Fed’s target range for its benchmark rate, and is also above today’s G/C overnight repo rate of 1.90%, with Alex Li, head of U.S. rates strategy at Credit Agricole, noting that elevated term rates are a problem because of the quantity of capital at risk.

Third, the reason why the Fed was likely forced to launch term repo, is because while investors have called for measures that will permanently boost reserves, such as POMO/QE, the Fed has so far refrained from embarking on a longer-term solution to ease the funding stress, writes Bloomberg’s Elizabeth Stanton. Specifically, Chair Powell said after Wednesday’s policy decision that he didn’t see “any implications for the broader economy” from the repo crunch, which prompted traders to exit long basis trades – long positions in Treasuries hedged with shorts in futures – which normally perform well when the Fed is cutting rates. “Futures outperformed cash amid the spike in repo and in the wake of an FOMC that could have done more to instill confidence in its attention to the issue,” Credit Suisse strategist Jonathan Cohn said. “The move flushed out significant long basis positioning.”

In short, despite the generous use of the $75 billion overnight repo, it wasn’t enough, and STIR and repo traders were spooked enough to force the Fed to engage in yet another form of liquidity injection, in the form of term repos.

From a robust mintage of 1.2 million pieces, the 1879-S Liberty double eagle was heavily circulated at the time of issue and many examples were used to settle large accounts in foreign trade. Many coins have been repatriated from overseas holdings in recent years, but most examples seen have excessive bag-marks from rough storage and transport. Mint State coins are scarce in today’s market and high-grade examples are rare.

We have six coins available…

Offered at $2,150 each delivered

We do business the old fashioned way, we speak with you.

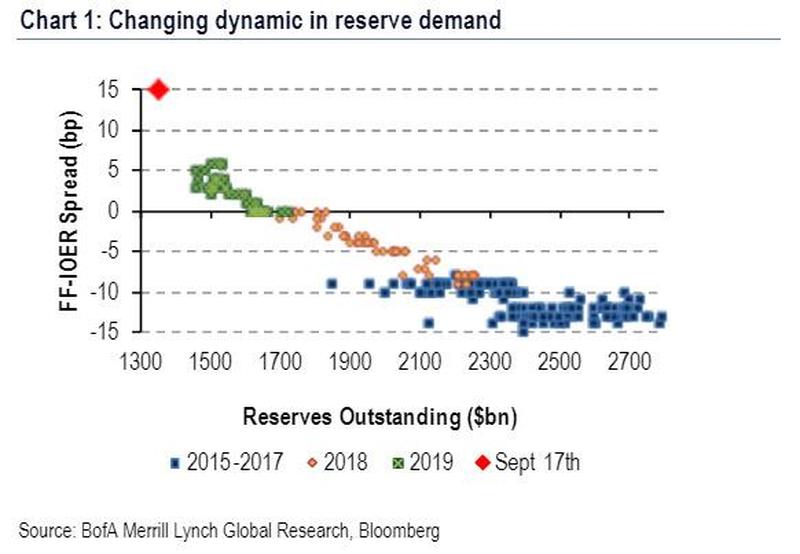

One of the reasons for the sharply hawkish response to yesterday’s FOMC meeting – one which saw both the dollar and yields spike – is that as we pointed out yesterday morning, in the hours ahead of Powell’s press conference, Wall Street consensus quickly shifted with many expecting the Fed to announce some form of permanent repo facility or restart of POMO (or QE for those who call a spade a spade) to push reserves back to a level where the funding market is stable. This, as we showed with the following chart, would require some $400 billion in new reserves for the FF-IOER spread to normalize.

To the disappointment of many, Powell did not do that, and instead, the FOMC realigned both interest on excess reserves (IOER) and the reverse repo (RRP) rate lower by 5bp, resulting in 30bp cuts to both rates. Powell also noted during his press conference that the Fed would use temporary open market operations (OMOs) “for the foreseeable future” to address pressures in funding markets.

However, and the reason why stocks shot up just before 3pm ET, is that that’s when Powell added that “it’s possible that we’ll need to resume the organic growth of the balance sheet, earlier than we thought. … We’ll be looking at this carefully in coming days and taking it up at the next meeting” in late October. Said otherwise, the Fed may not have announcer QE4 yesterday, but it will likely announce it in the very near future.

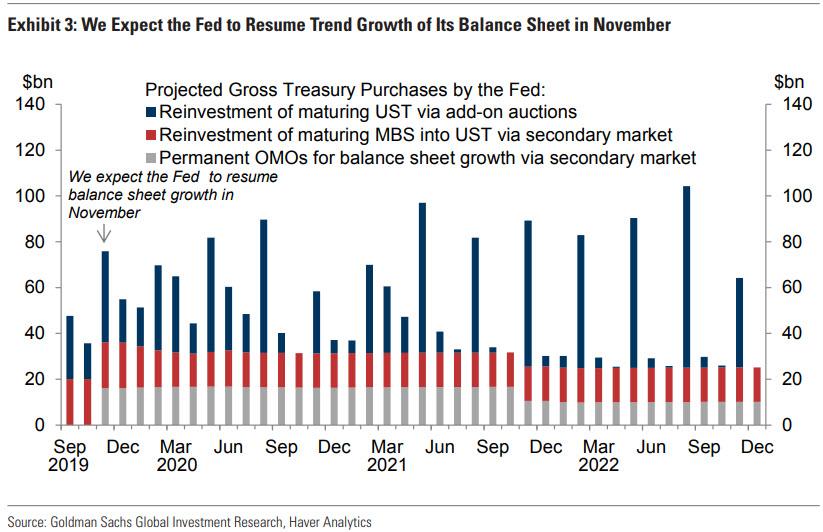

Sure enough, as Goldman wrote in its FOMC post-mortem, “we took this as a fairly strong hint and now expect the Fed to resume trend growth of its balance sheet in November with permanent OMOs. It is possible that the FOMC will take that opportunity to also reach a final decision on possibly shortening the maturity composition of its purchases, which it discussed at its May meeting.”

So what will the Fed’s restart of QE POMO (some analysts, such as Morgan Stanley’s Matt Hornbach are very sensitive not to call the return of POMO as QE even though both are effectively the monetization of US Treasurys and the US budget deficit) look like?

In the chart below, Goldman summarizes its projections of the Fed’s future gross Treasury purchases. The blue bars show reinvestment of maturing UST, which occur via add-on Treasury auctions. The red bars show reinvestment of maturing MBS, which occur via the secondary market.

The grey bars are where things get fun as they show permanent OMOs to support trend growth of the Fed’s balance sheet, which will occur via intervention of the Fed’s markets desk in the secondary market.

Here, similar to Bank of America, Goldman assumes a roughly $15bn/month rate of permanent OMOs, enough to support trend growth of the balance sheet plus some additional padding over the first two years to increase the size of thebalance sheet by $150bn, restoring the reserve buffer and eliminating the current need for temporary OMOs.

That strategy would result in balance sheet growth of roughly $180bn/year and net UST purchases by the Fed (the sum of the red and grey bars) of roughly $375bn/year over the next couple of years.

And so, in just two months QE… pardon the Fed’s open market purchases of Treasuries, will return after a 5 years hiatus. Just don’t call it QE, whatever you do.

The 1882-O eagle is an elusive issue from a small mintage of 10,820 coins. The average survivor grades AU50. Rarely encountered in Mint State, with fewer than 40 pieces certified MS60 to MS63 at PCGS and NGC combined. This particular example is particularly flashy with semi-prooflike surfaces and a bold strike. Listed at $12,100 in the CDN CPG and $11,800 in the NGC price guide.

Offered at $10,575 delivered

We do business the old fashioned way, we speak with you.

The 1852-C is among the most plentiful Charlotte gold dollar issues despite a mintage of only 9,434 coins. Doug Winters estimates that as many as 350 coins may survive. However, few are in the upper Mint State grades. This Plus-graded near-Gem is conditionally rare, and just a few finer pieces are reported. It is the only MS64 coin at NGC with a Plus designation. This particular example is highly lustrous, displays lovely color and boasts strong overall eye-appeal. Listed in the NGC price guide at $17,500 in MS64 condition and unlisted in MS64+. Only 6 have been graded higher by NGC.

Offered at $16,995 delivered

We do business the old fashioned way, we speak with you.